1200×675 PNGs (16:9, optimized for Twitter / LinkedIn / Slack preview cards). Updated weekly. CC BY 4.0 with attribution. No interview required to use.

Required attribution: “Source: Della Vedova Prediction Market Indices (DV-PMI), jdellavedova.com.” All charts derived from 671M on-chain Polymarket records since November 2022.

All quotes released under CC BY 4.0; edit freely as long as attribution remains.

Oracle tampering ('outsider trading') in prediction markets

“Whether the confidence comes from an inside line or a rigged sensor, it shows up the same way: accuracy the market's own prices cannot explain. Screening for excess accuracy catches both. And no market should resolve from a single number at a single source.”

From The Atlantic (July 20, 2026), on the Paris 'hair-dryer incident': the excess-accuracy method built for insider detection also flags traders who alter outcomes rather than forecast them.

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: The Atlantic, 'The ‘Hair-Dryer Incident’ Is Just the Start' (July 20, 2026).

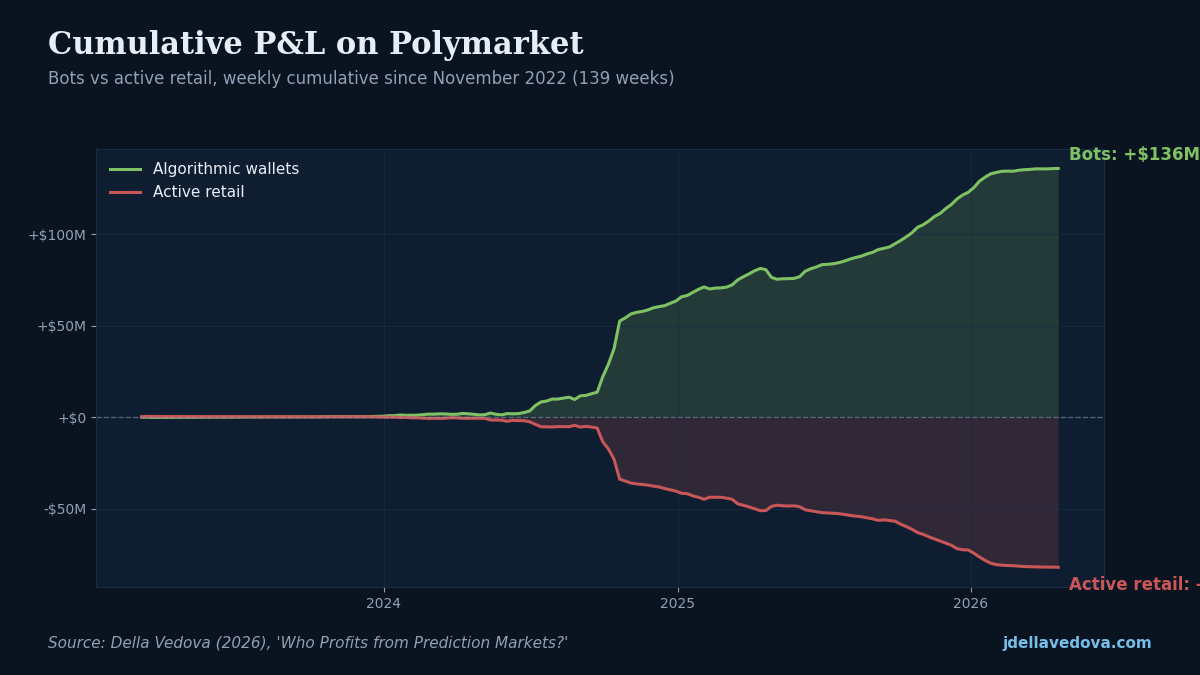

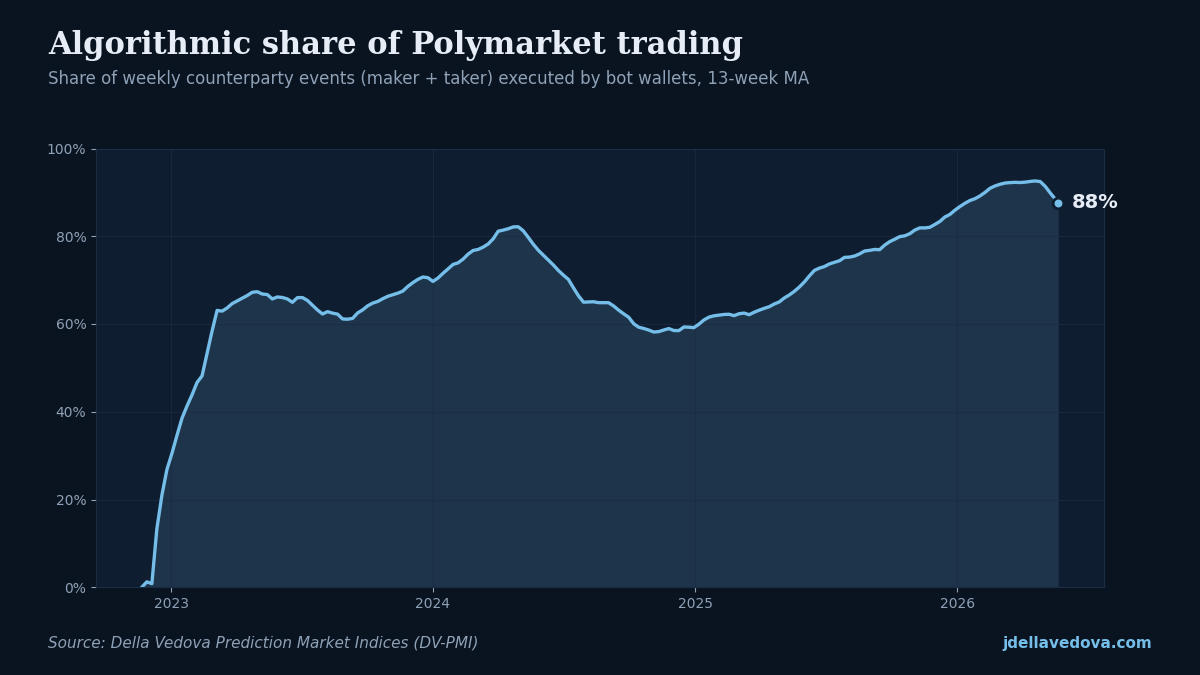

Algorithmic dominance of Polymarket volume

“Bots now capture nearly every dollar of volume on Polymarket, up from about half two years ago. The retail trader's share of the market is vanishing.”

From Paper 1 and the weekly Bot Share of Volume index: bots execute 94% of weekly trades in recent weeks.

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: Della Vedova (2026), 'Who Profits from Prediction? Execution, not Information.'

Informed trading detection in prediction markets

“Most of what looks like insider trading in prediction markets is just skill. Tested trader by trader, about one wallet in a hundred beats the market persistently; that is a skill signature, not evidence of inside information. Tested event by event, with every statistical correction applied, the entire history of Polymarket yields eleven trader-event pairs whose patterns are consistent with episodic private information, and on markets where inside information is implausible the test finds none at all.”

From Paper 2 (June 2026 revision): 4,657,827 testable trader-event pairs across 1,020,455 traders; 1,008 raw flags reduce to a 112-pair distinct-question core; 11 survive the within-event dependence adjustment at the 5% level (0 at 1%); zero corrected discoveries on the 597,146-pair placebo class.

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: Della Vedova (2026), 'Detecting Informed Trading in Prediction Markets: One Event at a Time,' SSRN abstract 6567238, revised June 2026.

Human traders and probability weighting

“Human traders on Polymarket distort probabilities in exactly the way Tversky and Kahneman predicted in 1992. The weekly pattern is visible, measurable, and remarkably stable.”

From Paper 4 (in progress): non-bot Prelec alpha averaged roughly 0.65 across 150 weeks, matching the canonical experimental estimate.

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: Della Vedova and Grant (2026, in progress), 'Probability Weighting from Prediction Markets.'

How much money does informed trading actually make?

“The headline-grabbing number is not the right one. The defensible core of informed trading we can identify on Polymarket earned about half a million dollars, concentrated in a handful of disclosure events. The bigger market-integrity finding is what the corrected test rules out: on markets where inside information is implausible, it finds nothing at all.”

From Paper 2 (June 2026 revision), Table 8: net directional profit across the 74 distinct-question core pairs with position coverage is $501,167 (median $778 per pair; the largest single case accounts for 55%).

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: Della Vedova (2026), 'Detecting Informed Trading in Prediction Markets: One Event at a Time,' SSRN abstract 6567238, revised June 2026.

Two-dimensional trading skill

“Trading skill in prediction markets is two-dimensional. Forecasting accuracy and execution quality are different capacities drawing on different resources, and they are nearly uncorrelated at the trader level. Execution, not forecasting, is what determines who profits.”

From Paper 1. Bots achieve coin-flip forecasting accuracy (49.9%) yet earn positive returns via execution; active retail achieves 51.3% accuracy but loses money due to poor execution.

Joshua Della Vedova, Associate Professor of Finance, University of San Diego. Source: Della Vedova (2026), 'Who Profits from Prediction? Execution, not Information.'

Upcoming and recent talks will appear here.

Joshua Della Vedova is an Associate Professor of Finance at the Knauss School of Business,

University of San Diego. His research on prediction markets draws on 671 million on-chain

Polymarket records (222 million resolved trades). See the research page for working papers, the

methodology page for index construction, and the

DV-PMI dashboard for live indices.

Quotes are released under Creative Commons Attribution 4.0. Attribution line included with each quote is the minimum citation; journalists are welcome to edit for length or style as long as the attribution remains.